The world’s largest decentralized lending protocol, Aave, is currently grappling with a localized "bank run" scenario. On the Ethereum mainnet, utilization for the two most critical stablecoins, USDC and USDT, have pinned at 100%. This means every single dollar deposited into these pools is currently being borrowed, leaving the "available liquidity" at zero and lenders unable to withdraw their assets.

Why Can't I Withdraw from Aave?

If you are currently attempting to withdraw USDC or USDT from Aave and receiving errors, it is because utilization has reached 100%. In DeFi lending, you can only withdraw if there is "idle" capital in the pool. When all funds are utilized by borrowers, lenders must wait for someone to repay their loan or for new deposits to enter the pool. This is a classic liquidity trap, currently exacerbated by a new interest rate model.

The 'Slow Burn' & Slope2 Risk Oracle

To understand why this crisis is persisting, we must look at the Slope2 Risk Oracle. Historically, Aave used a "kinked" interest rate model. Once utilization passed a certain threshold (e.g., 90%), the interest rate would spike instantly to 80%+ APY to force borrowers to repay.

The new Slow Burn mechanism, managed by the Aave Generalized Risk Stewards (AGRS), changes this. Instead of an instant spike, the Slope2 parameter escalates rates gradually over a 24 to 72-hour window. Currently, many of these rates are capped at a modest 10-12% during the initial escalation phase.

What Happened to DeFi Users: Lenders Frozen, Attackers Protected

The "Slow Burn" was designed to prevent volatile "flash" liquidations, but in a crisis, it creates a massive imbalance of power:

For Borrowers: An attacker or institutional borrower sitting on hundreds of millions in debt is essentially paying a "cheap" interest rate (12%) to keep the liquidity trapped.For Lenders: Users are not being compensated for the risk. While their funds are frozen, they are earning a fraction of the market "risk premium" because the oracle prevents the rate from hitting the necessary 80%+ to force a repayment.Institutional Flight: The $8B Deposit Exodus

The lack of immediate liquidity has triggered a massive loss of confidence. Data suggests an estimated $8 billion deposit flight from the ecosystem. Major players like Abraxas Capital and users on exchanges like MEXC have moved aggressively to pull assets. Those who did not exit before the 100% utilization mark are now locked in, watching the "Slow Burn" play out in slow motion.

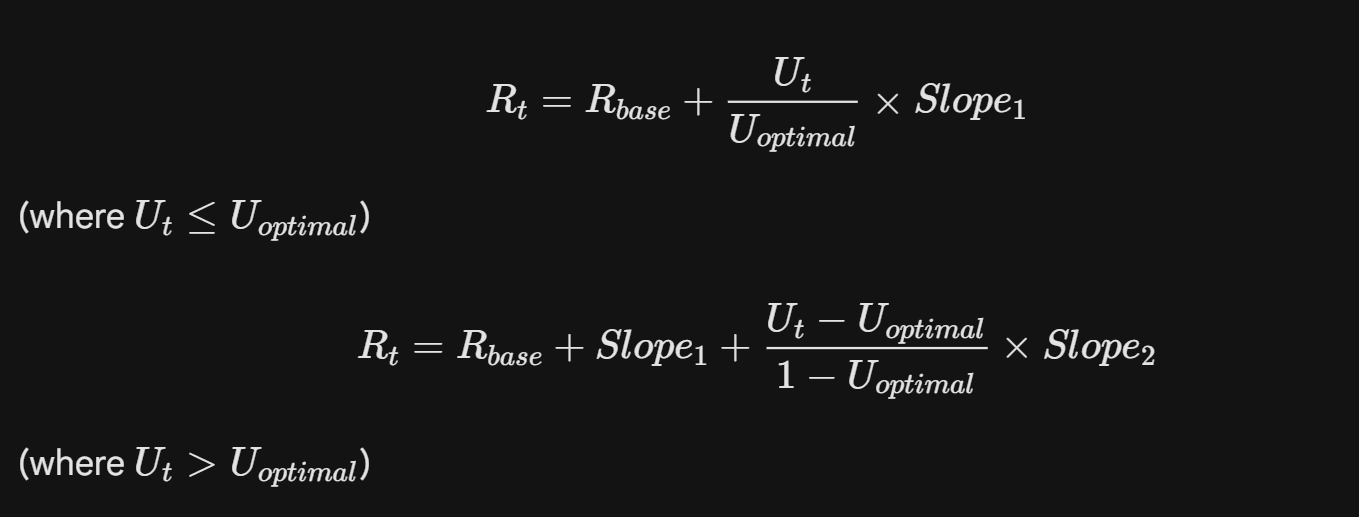

Technical Structure: How the Slope2 Math Works

In technical terms, the Variable Borrow Rate (Rt) is calculated using the following logic:

In this crisis, the Slope2 value is no longer a fixed constant but a dynamic variable that climbs slowly. This "wait-and-see" approach by the protocol has turned what should have been a 1-hour liquidity crunch into a multi-day crisis.

What's going to Happen to DeFi Users?

For now, retail lenders in USDC and USDT pools must wait for the "Slow Burn" to eventually reach a punitive level—likely above 50%—to force borrowers to return the funds. This event serves as a cautionary tale regarding the trade-offs between "smooth" interest rate curves and protocol protocol agility during black swan events.

Bengali (Bangladesh) ·

Bengali (Bangladesh) ·  English (United States) ·

English (United States) ·